Estate Planning Isn’t Boring: How Wealth Transfer Can Be About Legacy

Estate planning has a terrible reputation. Most Australians think it’s about death, taxes, and tedious paperwork. They imagine stuffy lawyers’ offices filled with dusty legal documents. The whole process feels morbid and overwhelming.

This perception is completely wrong and it’s costing families their most meaningful opportunities.

Estate planning isn’t about death. It’s about life continuing beyond your physical presence. It’s about ensuring your values, wisdom, and impact live on through the people you love most. It’s about creating something bigger than yourself that spans generations.

The families who understand this transform estate planning from a dreaded chore into an inspiring family project. They use wealth transfer as a tool for connection, education, and empowerment. They create legacies that matter long after bank accounts are settled.

Disclaimer: This article is for general information only. It does not constitute legal, tax, or financial advice. Seek advice from a qualified professional before making decisions about estate planning or wealth transfer.

Why Estate Planning Feels Dull

The estate planning industry has done itself no favours with its messaging and approach. Traditional advisers focus on minimising taxes and avoiding probate. Legal documents get written in incomprehensible jargon. The entire process feels like preparing for failure rather than celebrating success.

Australian families absorb these negative associations and naturally procrastinate. Who wants to spend weekends thinking about death certificates and executor duties? The cultural messaging around estate planning emphasises loss, complexity, and bureaucracy rather than opportunity and empowerment.

This framing problem has real consequences. Brilliant parents die without sharing their life lessons with their children. Successful business owners leave no guidance for the next generation. Family wealth dissipates because nobody prepared the heirs for their responsibilities.

The “box-ticking” stereotype

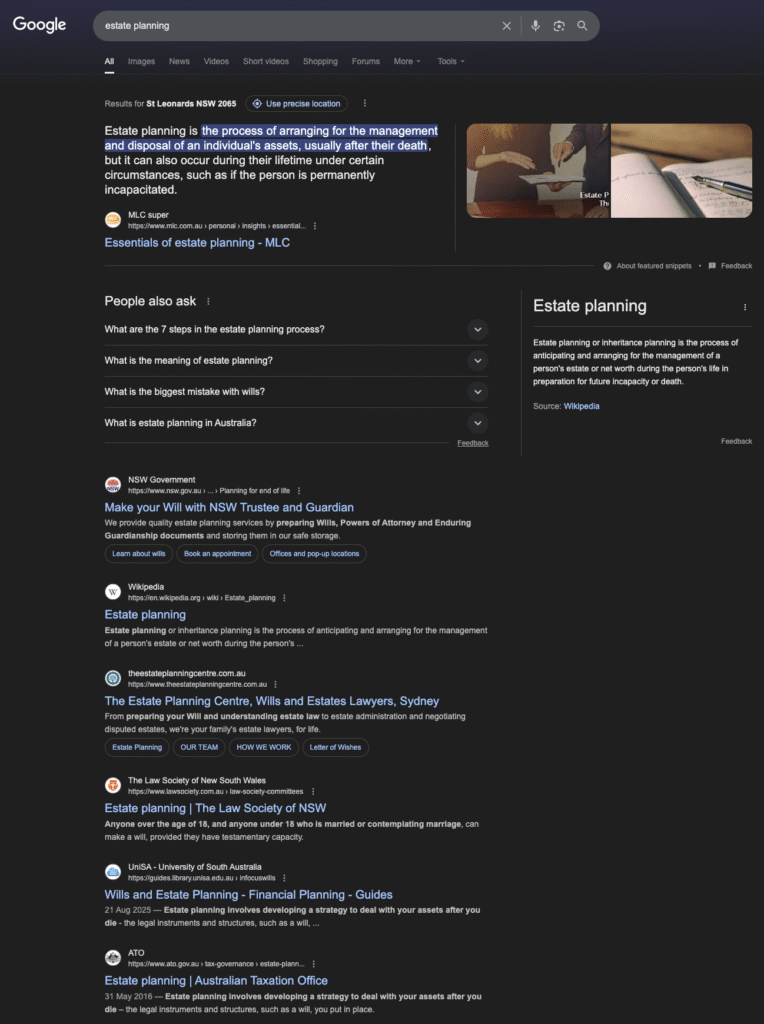

Don’t believe estate planning has a boring problem? Try this simple test. Go to Google and search for “estate planning Australia.” Look at the first page of results.

Five out of ten results are law firms with identical messaging about “protecting your assets” and “avoiding probate complications.” Their websites feature stock photos of elderly couples looking worried about paperwork. The content focuses on legal technicalities and tax minimisation strategies.

The remaining results? Government agencies, Universities and the Australian Taxation Office explaining compliance requirements. More forms, more bureaucracy, more reasons to procrastinate.

This is what families see when they first explore estate planning. No wonder they think it’s boring.

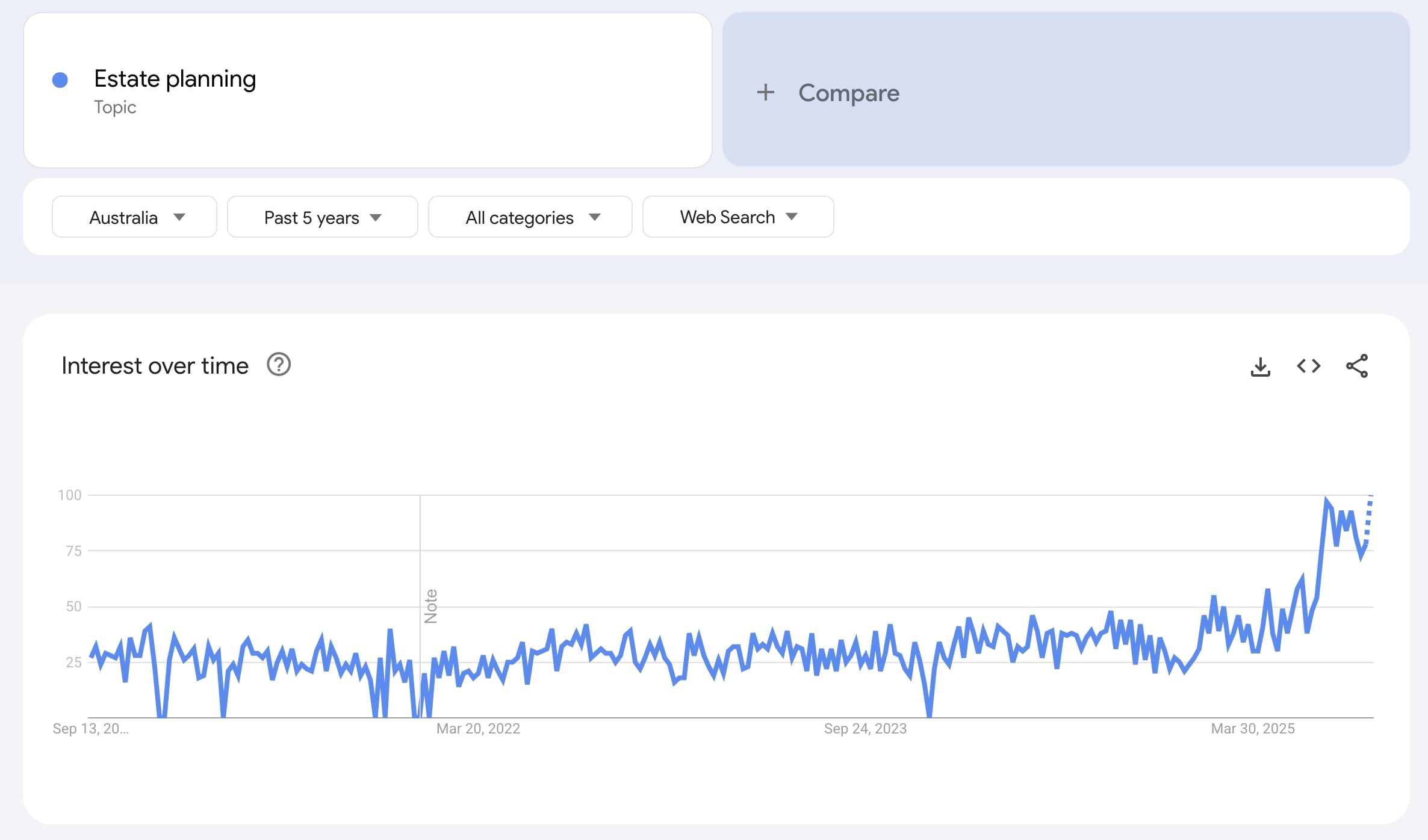

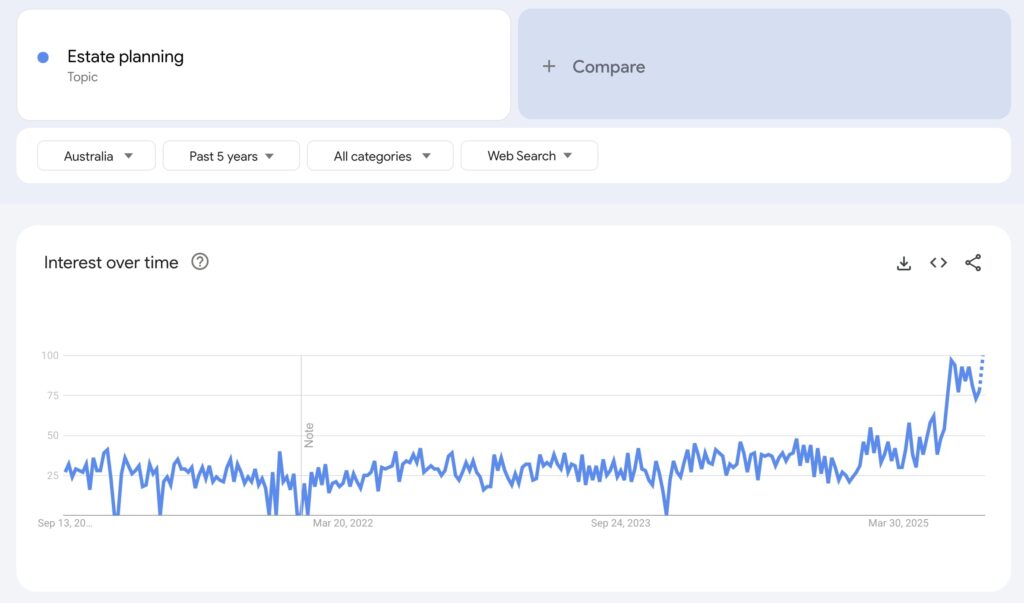

Yet here’s what’s fascinating: Google Trends data shows Australian interest in “estate planning” is at an all-time high. Australians are searching for estate planning information more than ever before.

The demand exists. The interest is there. But the supply side (boring law firm websites and government compliance guides) isn’t meeting what families actually want.

Traditional estate planning follows a predictable checklist approach. Write a will. Choose an executor. Set up a trust if your assets justify the complexity. Review beneficiary designations on superannuation accounts. Update everything when circumstances change.

This mechanical process strips away the human elements that make estate planning meaningful. It reduces decades of life experience to legal formalities. It treats family relationships as simple asset allocation decisions. No wonder people find it boring.

The box-ticking mentality also creates a false sense of completion. Families think they’re “done” with estate planning once documents are signed and stored. They miss the ongoing conversations, education, and relationship building that create lasting legacies.

Real estate planning never ends because families never stop growing and evolving. Children mature into adults with their own values and goals. Business circumstances change. New opportunities emerge for impact and connection. Static documents can’t capture this dynamic reality.

The most engaged families treat estate planning as an ongoing family dialogue rather than a one-time legal exercise. They regularly discuss values, expectations, and opportunities. They involve multiple generations in planning conversations. They use wealth transfer as a catalyst for deeper relationships.

Association with death and bureaucracy

Marketing materials for estate planning services are filled with grim reminders about mortality. “Don’t leave your family in chaos.” “Avoid the probate nightmare.” “Protect your assets from unexpected death.” These messages create anxiety rather than inspiration.

Death is certainly part of estate planning, but it’s not the central theme. The central theme is continuation; ensuring that your influence, values, and care for family members continues after your physical presence ends. That’s actually quite beautiful when framed properly.

Bureaucratic complexity adds another layer of discouragement. Legal forms use archaic language that normal people can’t understand. Government requirements seem designed to frustrate rather than facilitate family planning. Professional fees can be substantial without clear value demonstration.

Modern estate planning doesn’t have to be bureaucratic or intimidating. Technology platforms simplify document creation and management. Plain English explanations replace legal jargon. Digital tools make complex concepts visual and understandable. The experience can be engaging rather than overwhelming.

The death association also prevents families from engaging early enough. Young parents think estate planning is for older people. Successful professionals postpone planning until health scares motivate action. By then, opportunities for family education and preparation are missed.

Cultural and generational perceptions in Australia

Australian cultural attitudes toward wealth and planning create additional barriers to engagement. The tall poppy syndrome discourages open discussion about family assets. Privacy concerns prevent intergenerational conversations about inheritance expectations. Many families consider wealth discussions inappropriate or presumptuous.

Generational differences complicate family planning conversations. Baby Boomers accumulated wealth through property investment and superannuation growth. Generation X focuses on work-life balance and experiences over assets. Millennials prioritise sustainability and social impact over traditional wealth accumulation.

These different value systems can create tension during estate planning conversations. Older generations worry that younger family members don’t appreciate hard work and frugality. Younger generations question whether traditional wealth accumulation aligns with their values and priorities.

Cultural diversity adds another layer of complexity to Australian estate planning. Different ethnic communities have varying traditions around family wealth, elder care, and intergenerational responsibility. Blended families create complicated relationships that don’t fit standard legal templates.

The families who succeed in creating meaningful legacies embrace these cultural complexities rather than ignoring them. They facilitate open conversations about different perspectives and values. They find common ground while respecting individual differences. They use estate planning as an opportunity to strengthen rather than strain family relationships.

Legacy as Opportunity

The most inspiring estate planning conversations focus on opportunity rather than obligation. They explore how wealth transfer can amplify family values and create lasting impact. They examine how financial resources can enable dreams and aspirations across generations.

This shift in perspective transforms everything about the planning process. Instead of minimising taxes, families maximise opportunity. Instead of avoiding problems, they create solutions. Instead of preparing for death, they design for life continuation and expansion.

Legacy-minded families ask different questions during planning conversations. What values do we want to perpetuate? How can we prepare the next generation for their responsibilities? What impact do we want to have beyond our immediate family? These questions generate energy and engagement rather than anxiety and avoidance.

Shaping family continuity and values

Family values often get lost during traditional estate planning because the focus stays on asset allocation rather than character development. Wills specify who gets what but ignore who the recipients are becoming. This creates inheritance without preparation – a recipe for family conflict and wealth dissipation.

Values-based estate planning integrates character development with wealth transfer. Parents articulate the principles that guided their success. They create systems for passing wisdom along with assets. They design inheritance structures that reinforce positive behaviours and discourage destructive ones.

Consider how this works in practice. A family business owner might establish mentorship requirements before ownership transfer. Parents could create educational incentives for grandchildren’s development. Philanthropic commitments might reflect family values around social responsibility and community contribution.

These approaches ensure that family wealth serves family values rather than undermining them. Money becomes a tool for character development and family connection. Inheritance becomes an opportunity for growth rather than a windfall that creates entitlement or dysfunction.

The most successful multigenerational families create formal systems for values transmission. Family constitutions articulate shared principles and expectations. Regular family meetings provide forums for discussion and decision-making. Educational programmes prepare younger generations for their roles and responsibilities.

Empowering heirs through preparation and awareness

Traditional estate planning often keeps heirs in the dark until inheritance actually occurs. Parents worry that knowledge about future wealth will reduce children’s motivation to develop their own capabilities. This well-intentioned secrecy often backfires by creating unpreparedness and family tension.

Preparation-focused families take the opposite approach. They gradually increase heirs’ knowledge and responsibility over time. They provide education about family wealth, business operations, and philanthropic activities. They create opportunities for younger generations to demonstrate readiness and earn trust.

This transparency serves everyone’s interests. Parents gain confidence that their values will continue after their deaths. Heirs develop the skills and perspective needed for responsible wealth stewardship. Family relationships strengthen through open communication and shared purpose.

Preparation involves more than financial education. Heirs need to understand family history and the sacrifices that created current wealth. They need exposure to different perspectives on money, success, and responsibility. They need practice making decisions with real consequences before inheriting significant resources.

The best family preparation programmes combine formal education with practical experience. Young family members might intern in family businesses, serve on nonprofit boards, or manage smaller investment portfolios. These experiences build capability while demonstrating commitment to family values.

Leaving an impact beyond financial assets

Financial wealth represents just one dimension of family legacy. Intellectual capital, social connections, and values often matter more than bank account balances. Families that understand this create more meaningful and durable legacies.

Intellectual capital includes the knowledge, skills, and wisdom that family members have developed over time. Business insights, investment experience, and life lessons often have more value than the assets themselves. This knowledge disappears unless families systematically capture and transfer it.

Social capital encompasses the relationships and reputation that families build within their communities. Professional networks, philanthropic connections, and community standing can provide opportunities and resources for future generations. These relationships require intentional cultivation and transfer.

Values capital represents the principles, character traits, and cultural elements that define family identity. These intangible assets influence how family members approach challenges, opportunities, and relationships. They determine whether financial wealth enhances or diminishes family wellbeing over time.

The families with the strongest legacies invest as much energy in developing these intangible assets as they do in accumulating financial wealth. They document family stories and business histories. They introduce younger generations to important relationships. They create systems for reinforcing values and character development.

Modern Tools Make It Engaging

Technology is transforming estate planning from a document-driven process into an interactive family experience. Digital platforms make complex concepts visual and understandable. Collaboration tools enable participation from family members across different locations and time zones. Modern approaches engage people who would never sit through traditional planning sessions.

These technological advances address many of the traditional barriers to estate planning engagement. Complexity becomes manageable through user-friendly interfaces. Geographic distance doesn’t prevent family participation. Younger generations can engage through familiar digital platforms rather than intimidating legal offices.

The most innovative families are using technology not just for efficiency but for education and engagement. They create digital family histories that capture stories and values. They use visualisation tools to explore different planning scenarios. They build online platforms for ongoing family communication and collaboration.

Digital planning platforms, collaboration tools, and recordkeeping

Modern estate planning platforms transform the traditional document creation process into interactive family workshops. Instead of passive receipt of legal documents, families actively explore different scenarios and their implications. They can model various distribution approaches and see the results immediately.

Collaboration tools enable meaningful participation from family members who can’t attend in-person meetings. Adult children living in different states can contribute to planning conversations through video conferencing. Grandchildren can share their perspectives through secure online platforms. Geographic barriers no longer prevent inclusive family planning.

Digital recordkeeping solves many traditional estate planning headaches. Important documents don’t get lost in filing cabinets. Version control prevents confusion about current instructions. Access controls ensure appropriate people have necessary information when needed. Backup systems protect against loss or damage.

These platforms also facilitate ongoing communication about estate planning topics. Families can share articles, discuss scenarios, and update information between formal planning sessions. The planning process becomes continuous rather than episodic. Relationships strengthen through regular interaction and shared learning.

Security and privacy protections ensure that sensitive family information remains confidential while enabling appropriate access. Multi-factor authentication prevents unauthorised access. Encryption protects data during transmission and storage. Audit trails track who accessed what information and when.

Visualising estates and wealth transfer for families

Visual tools make abstract estate planning concepts concrete and understandable. Family tree diagrams show how assets flow between generations. Timeline graphics illustrate when different planning strategies take effect. Scenario modelling demonstrates the long-term impact of various decisions.

These visualisations particularly benefit younger family members who learn better through interactive media than traditional lectures. Complex trust structures become understandable through flowcharts and diagrams. Tax implications become clear through before-and-after comparisons. Family governance structures make sense through organisational charts.

Interactive calculators help families explore “what if” scenarios without commitment. They can model different giving strategies and see the impact on family wealth. They can explore various business succession approaches and understand the trade-offs. They can experiment with different distribution timelines and evaluate the implications.

Virtual reality and augmented reality technologies are beginning to enhance estate planning education. Families can “walk through” different planning scenarios and experience the results. They can visualise how business succession might unfold over time. They can explore the long-term implications of various philanthropic strategies.

Gaming elements make estate planning education more engaging for younger participants. Points, badges, and progress tracking encourage participation in family planning activities. Simulation games help people understand the consequences of different financial decisions. Interactive quizzes test knowledge and reinforce learning.

Making planning practical across generations

Multi-generational planning requires tools and approaches that work for different age groups, technology comfort levels, and learning styles. Traditional estate planning typically focuses on the wealth creators while neglecting the perspectives and needs of wealth inheritors.

Modern planning platforms accommodate these generational differences through flexible interfaces and communication options. Older participants might prefer printed summaries and phone conversations. Younger participants might engage primarily through mobile apps and social media integration. Effective systems support multiple communication preferences simultaneously.

Educational content needs to be relevant and accessible to different generations. Baby Boomers might want detailed analysis of tax strategies and legal implications. Generation X might focus on work-life balance and family coordination. Millennials might prioritise social impact and sustainability considerations.

Practical planning tools help families bridge generational gaps through shared activities. Collaborative planning sessions give each generation voice in family decisions. Mentorship programmes pair older and younger family members for mutual learning. Joint philanthropy enables shared impact and relationship building.

Technology training helps older generations participate more effectively in digital planning processes. Younger family members can provide technical support while learning from elder wisdom and experience. These intergenerational learning exchanges strengthen relationships while advancing planning objectives.

The Psychology of Legacy

Understanding the psychological drivers behind estate planning engagement reveals why traditional approaches often fail. People don’t procrastinate because they’re irresponsible, they delay because current methods don’t connect with their deeper motivations and values.

Research in behavioural psychology shows that humans are naturally drawn to activities that provide meaning, connection, and positive impact. Traditional estate planning emphasises compliance, risk mitigation, and death preparation. These themes trigger avoidance rather than engagement because they don’t align with fundamental human desires for purpose and significance.

Legacy-focused approaches tap into more powerful psychological motivations. They frame estate planning as an opportunity to create lasting impact and strengthen family relationships. They emphasise growth, empowerment, and life continuation rather than loss, complexity, and bureaucracy.

People care more about impact than paperwork

Traditional estate planning prioritises legal compliance and tax optimisation over human impact and relationship building. This technical focus appeals to advisers but alienates the families who need to engage with the planning process. Most people care more about their influence on others than their influence on tax calculations.

Meaningful estate planning starts with impact rather than instruments. What difference do you want to make in the lives of people you care about? How can your resources and wisdom create opportunities for others? What legacy do you want to leave beyond financial distributions? These questions generate energy and engagement.

Impact-focused planning naturally leads to more sophisticated and effective strategies. Families who understand their desired impact can design systems to achieve those outcomes. They make better decisions about asset allocation, timing, and distribution methods. They create accountability systems that ensure their intentions become reality.

The most engaged families develop specific, measurable impact goals for their estate planning. They might want to enable grandchildren’s education, support family business development, or create lasting community benefits. These concrete objectives provide motivation for completing planning tasks and making difficult decisions.

Impact measurement helps families evaluate and improve their planning strategies over time. They track whether their approaches are achieving desired outcomes. They adjust methods based on results and changing circumstances. They create feedback loops that improve effectiveness and maintain engagement.

Teaching values, stewardship, and responsibility

Financial inheritance without character preparation often creates problems rather than opportunities. Young adults who receive significant wealth without adequate preparation may struggle with motivation, relationships, and personal identity. They may squander resources or become dependent rather than empowered.

Values-based estate planning addresses these risks through systematic character development and education. Parents articulate the principles that guided their success and create systems for reinforcing these values in the next generation. They design inheritance structures that reward positive behaviours and discourage destructive ones.

Stewardship education helps heirs understand their responsibilities as well as their privileges. Wealth creates opportunities to make positive impacts but also obligations to use resources wisely. Families that successfully transfer wealth across generations emphasise stewardship responsibilities alongside inheritance benefits.

Responsibility development happens through graduated experience with real consequences. Young family members might manage smaller investment accounts before inheriting larger sums. They might serve on nonprofit boards before joining family foundation leadership. They demonstrate readiness through actions rather than just age or relationship.

The most successful families create formal systems for values education and responsibility development. Family mission statements articulate shared principles. Mentorship programmes pair experienced and developing family members. Educational opportunities provide knowledge and perspective about wealth stewardship and family legacy.

Planning as a conversation, not a chore

Traditional estate planning treats families as passive recipients of legal and financial advice. Professional advisers develop recommendations based on technical analysis. Families review and approve strategies without deep engagement in the development process. This approach works for simple situations but fails for complex family dynamics.

Conversation-based planning invites families to actively participate in exploring their values, goals, and concerns. Multiple perspectives contribute to understanding and solution development. Different generations share their views about family priorities and planning approaches. These discussions often reveal insights that technical analysis would miss.

Regular family conversations about legacy topics prevent estate planning from becoming an overwhelming project that gets postponed indefinitely. Small, ongoing discussions are more manageable than comprehensive planning marathons. Families can explore topics gradually and build understanding over time rather than trying to address everything at once.

Conversation skills need development just like technical knowledge. Many families struggle to discuss money, death, and inheritance because they lack experience with these sensitive topics. Learning how to facilitate productive family discussions becomes an essential element of effective estate planning.

Professional facilitators can help families develop conversation skills and navigate difficult discussions. They provide neutral guidance when emotions run high or conflicts emerge. They ensure that all voices are heard and respected during planning processes. They help families build communication patterns that serve them well beyond formal planning sessions.

Reframing the Conversation

The language we use to describe estate planning shapes how people think and feel about the entire process. Words like “death planning,” “tax avoidance,” and “asset protection” create negative associations that trigger procrastination and disengagement. More inspiring language can transform perceptions and increase participation.

Legacy-focused language emphasises opportunity, growth, and positive impact rather than loss, compliance, and risk mitigation. This reframing doesn’t change the technical requirements of estate planning, but it dramatically changes how families experience and engage with the process.

Professional advisers who understand the power of language can help families reframe their thinking about estate planning. Instead of focusing on problems to avoid, they emphasise opportunities to create. Instead of dwelling on death and taxes, they explore life continuation and empowerment.

Language matters: “legacy” vs “death”

Compare these two approaches to the same estate planning conversation: “We need to discuss what happens to your assets when you die” versus “Let’s explore how your values and resources can continue creating impact through future generations.” Both address the same technical requirements, but they create completely different emotional responses.

Death-focused language triggers natural human avoidance mechanisms. Nobody wants to spend time thinking about their mortality and its implications. This biological programming served our ancestors well but creates problems for modern estate planning engagement. Families delay planning because the framing feels uncomfortable and depressing.

Legacy-focused language taps into positive human motivations around meaning, connection, and impact. People naturally want to make a difference in the world and the lives of people they care about. Estate planning becomes energising when framed as an opportunity to amplify rather than end their influence.

The shift from death planning to legacy creation changes everything about family engagement. Children become excited about continuing family traditions rather than anxious about inheritance conflicts. Parents feel motivated to share wisdom rather than overwhelmed by technical requirements. Grandparents see opportunities for connection rather than obligations for compliance.

Professional advisers who master legacy language serve their clients more effectively and build more sustainable practices. Families refer friends and colleagues to advisers who make planning inspiring rather than intimidating. Technical competence remains essential, but communication skills determine client satisfaction and business growth.

Encouraging participation from all generations

Traditional estate planning typically involves only the wealth creators and perhaps their adult children. Younger generations get excluded because they’re considered too young or uninterested. This approach misses opportunities for education, engagement, and relationship building across the entire family system.

Multi-generational planning requires age-appropriate participation from all family members. Young children can learn about family history and values. Teenagers can begin developing financial literacy and responsibility. Young adults can participate in planning conversations and decision-making processes.

Different generations contribute different perspectives to family planning discussions. Older generations provide wisdom, experience, and historical context. Younger generations offer fresh perspectives, technological expertise, and future-oriented thinking. Middle generations bridge different viewpoints and facilitate communication.

Inclusive planning processes strengthen family relationships and improve planning outcomes. When all generations participate in conversations, they develop shared understanding of family values and priorities. They build communication patterns that serve the family well during transitions and challenges.

Age-appropriate education helps different generations contribute meaningfully to family planning. Children learn through stories and activities rather than technical discussions. Teenagers benefit from real-world examples and hands-on experiences. Adults need comprehensive information and decision-making authority.

Removing fear and procrastination through perspective

Fear drives most estate planning procrastination. People worry about making mistakes with irreversible consequences. They fear family conflicts over inheritance decisions. They’re anxious about conversations with children about wealth and expectations. The research confirms this: 43% of Americans say they’ll wait until there’s a health crisis before creating estate plans.

This procrastination comes at an enormous cost. Without proper preparation, families destroy more wealth through poor transitions than market crashes or tax changes ever could. The statistics are unforgiving: only 12% of Australian family businesses survive to the third generation.

Perspective shifts can transform fear into excitement and procrastination into engagement. Estate planning becomes less intimidating when families understand that most decisions can be modified as circumstances change. Wills and trusts can be updated. Family communication can improve over time. Mistakes can be corrected through ongoing attention and adjustment.

The perfect estate plan doesn’t exist because families and circumstances constantly evolve. Children mature and develop their own values and priorities. Business conditions change. Investment markets fluctuate. Tax laws get modified. Effective planning embraces this uncertainty rather than trying to predict and control the future.

Starting with simple steps removes barriers to initial engagement. Families don’t need comprehensive estate plans before beginning meaningful conversations about values and priorities. They can explore topics gradually and build understanding over time. Small actions create momentum for larger planning initiatives.

Professional advisers can help families develop realistic perspectives about estate planning risks and opportunities. Technical mistakes are usually fixable through plan modifications. Family relationship problems often improve through better communication and shared planning activities. The risks of inaction typically exceed the risks of imperfect action.

Conclusion

Estate planning deserves better than its boring reputation. At its best, it’s one of the most meaningful projects families can undertake together. It creates opportunities for connection, education, and empowerment across generations. It transforms wealth transfer from a legal obligation into a legacy celebration.

The families who embrace this perspective discover that estate planning becomes energising rather than overwhelming. They use wealth transfer conversations to strengthen relationships and share wisdom. They create systems that perpetuate their values and amplify their impact long after their physical presence ends.

Modern tools and approaches make meaningful estate planning accessible to families who would never engage with traditional methods. Digital platforms remove barriers to participation and collaboration. Visual tools make complex concepts understandable. Legacy-focused language transforms perceptions and increases engagement.

Your family’s story doesn’t have to end with your death. With thoughtful planning and ongoing conversation, your influence can continue growing through the people and causes you care about most. That’s not boring – that’s the most important work you’ll ever do.

Disclaimer: This article is for general information only. It does not constitute legal, tax, or financial advice. Seek advice from a qualified professional before making decisions about estate planning or wealth transfer.